WEEK NINE AND TEN

TOPIC: SUBSIDIARY BOOKS

CONTENT

- Definition of Subsidiary Books

- Uses of the Subsidiary Books

- Preparation of the Subsidiary Books

- Transfer of the Totals of the Subsidiary books to the Ledger.

NOTES

Subsidiary books are the books of prime entry (or books of original entry) into which transactions are first recorded in details before they are posted in totals into the Ledger.

Businesses use subsidiary books to record goods sold on credit, goods purchased on credit, sales returns, purchases returns etc. The subsidiary books are basically listing devices, which means that a lot of detail is removed from the ledger. It also means that bookkeeping can be divided between several people. The name book of original (or prime) entry has arisen because all transactions should be recorded in one of these books before they are entered in the ledger.

The subsidiary books are:

- Sales Journal

- Purchases Journal

- Returns Inwards Journal

- Returns Outwards Journal

- General Journal

- Cash Book

- Petty Cash Book

Uses of the Subsidiary Books

- Sales Journal or Sales Day Book: This is used to record goods that are sold on credit to the customers of the business.

- Purchases Journal or Purchases Day Book: This is used to record goods bought on credit from the suppliers

- Return Inwards Journal or Returns Inwards Day Book: This is used to record goods returned by the customers to the business.

- Returns Outwards Journal or Returns Outwards Day Book: This is used to record goods returned by the business to suppliers.

- General Journal / Principal Journal / Journal Proper or The Journal: The general Journal has multiple uses.

Uses of the General Journal

- It is used to record opening entries.

- It is used to record closing entries.

- It is used to correct errors.

- It is used to record the purchase of fixed assets on credit.

- It is used to record the sale of fixed assets on credit.

- It is used to record one-off transactions.

- It is used to effect transfers of balances between ledgers.

- It is used to demonstrate the principle of double entry.

- It is used to record transactions that cannot be conveniently passed through any other subsidiary book.

- It is used to write off bad debts.

- It is used to record the purchase of business.

- It is used to record the issue, redemption and conversion of shares and debentures.

- Cash book: This is a subsidiary book of account that is used to record the receipt and payment of money (cash or cheque) to or by a business organization. The cash book is part of the double entry system. It functions both as a ledger and a subsidiary book of account.

- Petty Cash Book: This is the subsidiary book of account that is used to record the minor (low – value or petty) cash payments made by a business. Like the Cash Book, the Petty Cash Book is a subsidiary book and since it is part of the double entry system, it is also a ledger account.

EVALUATION

- What are books of prime entry?

- List eight uses of the General Journal.

Illustration

K. Laolu, a trader undertook the following transactions in the month of April 2016.

April 1 Started business with N25, 000 cash

” 2 Put N18, 000 of the cash into a bank account

” 5 Purchased from Co-operative Stores –

15 drums of groundnut oil at N20, 400 each

12 bags of garri at N3, 500 each.

Invoice subject to 10% trade discount

” 8 Sold to T. Okediran –

8 drums of groundnut oil at N24, 000 each.

Less 5% trade discount,

4 bags of garri at N4, 250 each

200 yams at N450 each

” 9 Returned to Co-operative Stores –

3 drums of groundnut oil bought on 5th April, 2016.

” 10 Bought from Oyesile & Sons –

650 yams at N380 each,

32 bags of onions at N12, 500 per bag,

60 bags of Dangote 50kg iodized salt at N3, 200 per bag.

” 12 Paid Co-operative Stores N65, 700 cheque on account

” 15 T. Okediran returned 3 drums of groundnut oil bought on the 8th of April, 2016.

” 18 Sold 320 yams at N550 each for cash

” 19 Bought from Ayodele & Co –

45 bags of onions at N12, 000 each,

50 cartons of Gino Tomato Paste at N14, 000 per carton,

20 drums of palm oil at N3, 800 per drum,

Invoice subject to 15% trade discount.

” 21 Returned to Ayodele & Co –

8 cartons of Gino Tomato Paste and 5 drums of palm oil bought on the 19th April, 2016.

” 22 Sold to Adjei Balama –

16 drums of palm oil at N4, 500 per drum,

20 bags of onions at N14, 000 each,

120 yams at N600 each,

Invoice subject to 5% trade discount

” 25 Paid sundry expenses N8, 400 by cheque

” 26 Paid rent of shop N15, 000 cash

” 27 Adjei Balama returned 5 drums of palm oil to us because they were damaged

” 29 T. Okediran paid by cheque for all the sales made to him.

” 30 Bought weighing machine from Standard Tools Ltd on credit N62, 000

You are required to record the above transactions in the appropriate books of original entry.

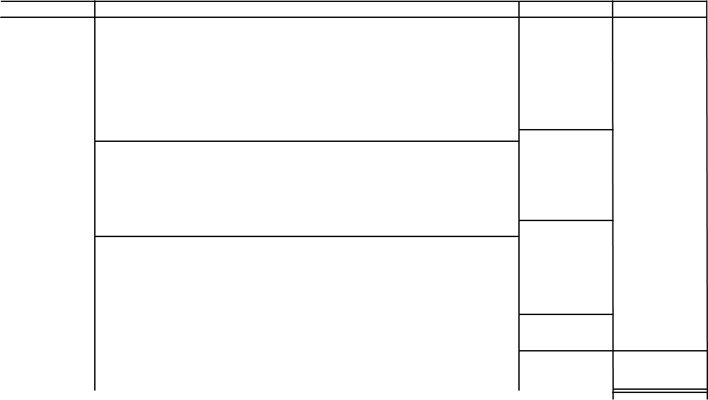

(a)

Cash Book

Cash Bank Cash Bank

Cash Bank Cash Bank

2016 N N 2016 N N

April 1Capital 25,000 April 2Bank c18,000

” 2 Cash c 18,000 “12 Co-operative stores 65, 700

” 18 Sales 176, 000 25 Sundry Expenses 8, 400

” 29 T, Okediran 221, 000″ 26 Rent 15, 000

![]() “30 Balance c/d 168,000 164, 900

“30 Balance c/d 168,000 164, 900

![]() 201, 000 239, 000 201, 000 239, 000

201, 000 239, 000 201, 000 239, 000

May 1 Balance b/d 168, 000 164, 900

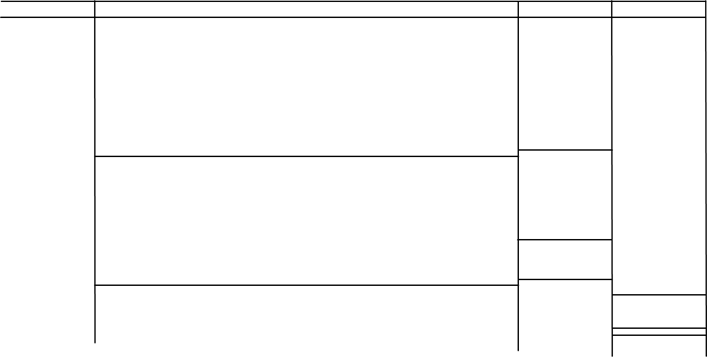

(b)

Purchases Journal

Purchases Journal

Date Narration Details Total

2016 N N

April 5 Co-operative stores –

15 drums of groundnut oil at N20, 400 each 306, 000

12 bags of garri at N3, 500 each 42, 000

![]() 348, 000

348, 000

Less 10% trade discount 34, 800 313, 200

April 10 Oyesile & Sons –

650 yams at N380 each 247, 000

32 bags of onions at N12, 500 per bag 400, 000

60 bags of Dangote 50kg iodized salt at N3, 200 per bag 192, 000 839, 000

April 19 Ayodele & Co. –

45 bags of onions at N12, 000 each 540, 000

50 cartons of Gino Tomato Paste at N14, 000 per carton 700, 000

20 drums of palm oil at N3, 800 per drum 76, 000

1, 316, 000

Less 15% trade discount 197, 400 1, 118, 600

Total Transferred to Purchases Account in the General Ledger 2, 270, 800

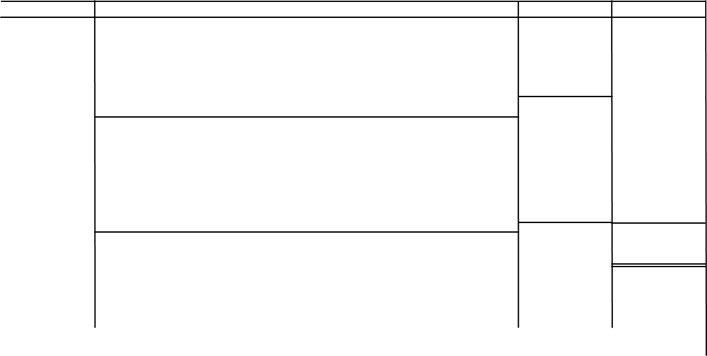

(c)

Sales Journal

Date Narration Details Total

Date Narration Details Total

2016 N N

April 8 T. Okediran

8 drums of groundnut oil at N24, 000 each 192, 000

Less 5% trade discount 9, 600

182, 400

4 bags of garri at N4, 250 each 17, 000

200 yams at N450 each 90, 000 289, 400

April 22 Adjei Balama –

16 drums of palm oil at N4, 500 per drum 72, 000 20 bags of onions at N14, 000 each 280, 000

120 yams at N600 each 72, 000

424, 000

Less 5% trade discount 21, 200 402, 800

Total Transferred to Sales Account in the General Ledger 692,200

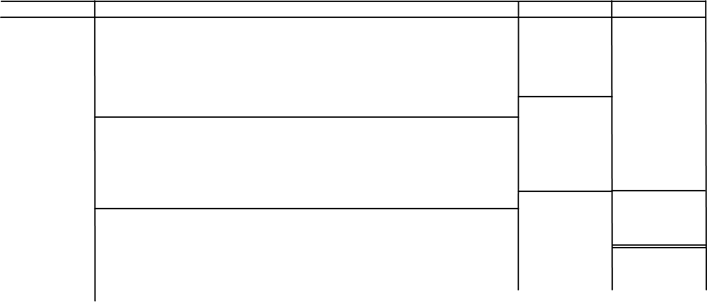

(d)

Returns Outwards Journal

Date Narration Details Total

2016 N N

April 6 Co-operative Stores –

3 drums of groundnut oil at N20, 400 each 61, 200

Less 10% trade discount 6, 120 55, 080

April 21 Ayodele & Co. –

8 Cartons of Gino Tomato Paste at N14, 000 per carton 112, 000 5 drums of palm oil at N3, 800 per drum 19, 000

![]() 131, 000

131, 000

Less 15% trade discount 19, 650 111, 350

Total Transferred to Returns Outwards Account in the 166, 430

General Ledger

(e)

Returns Inwards Journal

Date Narration Details Total

Date Narration Details Total

2016 N N

April 15 T. Okediran –

3 drums of groundnut oil at N24, 000 each 72, 000

Less 5% trade discount 3, 600 68, 400

April 27 Adjei Balama –

5 drums of palm oil at N4, 500 per drum 22, 500 Less 5% trade discount 1, 125 21, 375

Total Transferred to Returns Inwards Account in the 89, 775

General Ledger

(f)

General Journal

Date Narration Dr Cr

Date Narration Dr Cr

2016 N N

April 30 Equipment Account 62, 000

Standard Tools Ltd 62, 000

Being cost of weighing machine bought on credit

EVALUATION

- List seven books of original entry.

- State the use of each of the following.

(a) Sales Journal (b) Purchases Returns Journal (c) Petty Cash Book

GENERAL EVALUATION QUESTIONS

- What are books of prime entry?

- List any seven books of prime entry.

- State ten uses of the General Journal.

- Explain the principle of double entry.

- What is a source document?

WEEKEND ASSIGNMENT

- Which of the following is entered in the general journal? A. Purchase of good B. Sales of goods on credit C. Returns inwards D. Acquisition of fixed assets

- Which of the following subsidiary books involves cash movement? A. Sales Day Book

B. Purchases Day Book C. Returns Inwards Book D. Petty Cash Book

- Which of the following is an example of a subsidiary book? A. Cash book B. Bank statement C. Trial balance D. Suspense

- Which of the following is used to record the purchase of fixed asset on credit? A. Sales journal B. Purchases Journal C. Journal proper D. Cash book

- A sales journal is used to record A. Cash sales B. Credit sales C. Sales expenses D. Sales returns

THEORY

- State one advantage of sub-dividing the Journal into different classes.

- List ten books of account used in recording financial transitions of a business.