WEEK FOUR

ACCOUNTING RATIOS AND INCOMPLETE RECORDS

Under a situation whereby a firm or business accounting records were destroyed as a result of fire, flood or any other forms of natural disasters, such firm or business could still prepare its final account despite the facts that the information available will be very inadequate.

In order to prepare the final accounts under such situation, the accountant need to see his or her past experience and ingenuity to prepare the account. In addition, the accountant can make use of some accounting ratios such as the following:

- Mark – up

- Margin

- Rate of turnover

- Manager’s commission

Mark – up

This is the ratio that expressed profit against the cost price of goods. The profit will be expressed as a percentage or fraction or decimal to the cost price.

This is the ratio that expressed profit against the cost price of goods. The profit will be expressed as a percentage or fraction or decimal to the cost price.

Mark – up =

Illustration 5

A business made N10,000 profit from goods cost N50,000. You are required to calculate the mark-up.

Solution

Solution

Mark-up =

Mark-up =

=

= 20% or 0.2 or

Margin

This is the ratio of profit to sales or selling price. It can as well be expressed as a percentage or fraction or decimal to sales.

This is the ratio of profit to sales or selling price. It can as well be expressed as a percentage or fraction or decimal to sales.

Magin =

Illustration 6

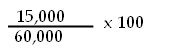

A firm made N15,000 profit from a sales of N60,000. You are required to calculate the margin.

Solution

Margin =

Margin =

=

= 2.5% or 0.25 or ¼

In a situation whereby the mark-up is given, as well as, the selling price then the mark-up must be converted to margin. This can be explained as follows:

SP = Selling price

CP = Cost price

Profit = P

SP = CP + P (i)

SP = CP = P (ii)

SP – P = CP (iii)

Mark-up = =

Margin = =

Conversion of mark-up to margin

Mark-up =

to margin =

=

Mark-up = to margin = =

Mark-up = to margin = =

Conversion of margin to mark-up

Margin = to mark-up = =

Margin = to mark-up = =

Margin = to mark-up =

=

Illustration 7

A business cost price is 100% and profit is 10%. Calculate mark-up and margin.

Solution

Mark-up = = = = 0.1

Margin = = = = = 0.091

Illustration 8

The following data were extracted from the books of God Grace Venture.

Opening stock 16,000

Sales 400,000

Closing stock 20,000

The business uses a uniform mark-up rate of 33 %

You are required to calculate:

- Profit

- Purchases

- Prepare the trading account

Solution

Mark-up 33 % =

Mark-up = = 25%

Margin = =

4P = 400,000

P = 400,000 ÷ 4

P = N100,000

Cost of sales = N400,000 – N100,000 = N300,000

![]() Purchase = 300,000 + 20,000 – 16,000 = N304,000

Purchase = 300,000 + 20,000 – 16,000 = N304,000

God Grace Trading Account

| N | N | |

| Sales Less: Cost of Sales Opening stock Add: Purchases Less: Closing stock Profit |

16,000 304,000 320,000 (20,000) | 400,000 |

Stock Turnover

This is also called the rate of turnover. This is the number of times a business stock will be turned over within a given period of time. It is computed as follows:

Rate of turnover = Cost of goods sold

Average of stocks

It can also be expressed in numbers of days as follows:

Average stocks (x 365 days)

Cost of goods sold

Average stock is computed as follows:

Opening stocks + Closing stocks

2

Manager’s Commission

This is an allowance granted to a business manager for a good performance and to encourage him or her to work harder in future. It is usually computed as follows:

Percentage of commission x Profit before commission

100 + Percentage of commission

Illustration 9

The following information was extracted from Folarin Ventures books in 2008.

| N | |

| Stock at 01/01/2008 Stock at 31/12/2008 Creditors at 01/01/2008 Creditors at 31/12/2008 Cash paid for goods during the year Mark-up 25% Selling expenses | 130,000 110,000 80,000 100,000 400,000 |

You are required to calculate:

- Margin

- Purchase

- Stock turnover in days

- Gross profit

- Sales

- Margin

- Prepare the trading, profit and loss account for the year ended 31 Dec. 2008.

Solution: FOLARIN VENTURES

- Margin = or = 20% or 0.2

- Purchase

Creditors Ledger Control Account

| N | N | ||

| Bal c/f Cash paid | 100,000 400,000 500,000 | Bal. b/f Purchases (credit) | 80,000 420,000 500,000 |

130,000 +110,000

![]() 2

2

![]() 440,000

440,000

![]() = 120,000

= 120,000

440,000

= 99.5 days = 100 days

Folarin Ventures

Trading and Profit and Loss Account for the period Ended 31 December 2008

| N | N | |

| Sales | 550,000 | |

| Opening stock | 130,000 | |

| Add: Purchase | 420,000 | |

| 550,000 | ||

| Less: Closing stock | ||

| 440,000 | ||

| Gross profit | 110,000 | |

| Less: Expenses | (55,000) | |

| Net profit | 55,000 |

Percentage of gross profit to sales = 110,000 x 100 = 20%

550,000

Percentage of Net profit to sales = 55,000 x 100 = 10%

550,000

Illustration 10

Madam Adeotun produces the following data from her books.

N

Stock at the beginning 30,000

Purchases 27,000

The mark-up on cost of sales is 50%. Her average stock during the year was N20,000. You are required to calculate:

- Closing stock

- Prepare trading, profit and loss account

- Ascertain the total amount of profit and loss expenditure that she must not exceed if she is to maintain a net profit on sales of 10%

Solution

Let x represent closing stock

- Closing stock = x + 30,000 = 20,000

2

= x + 30,000 = 40,000

= 40,000 – 30,000

Closing stock = x = N10,000

- Madam Adeotun Trading, Profit and Loss Account

N N Sales (290,000 + 145,000)

Less: Cost of sales

Opening prayer

Add: PurchasesLess: Closing stock

Gross profit (0.5 x 290,000)

Less: Expenses

Net profit (0.1 x 435,000)

30,000

270,000

300,000

(10,000)

435,000

290,000

145,000

(101,500)

43,500

43,500Exercise

Objective Questions

- A firm’s average stocks is N50,000 while the closing stock is N30,000. Calculate the opening stock:

- N40,000

- N30,000

- N70,000

- N50,000

- The ratio between profit and sales is called

- Gross profit

- Net profit

- Mark-up

- Margin

- The excess of opening capital over closing capital represents

- Gross profit

- Net profit

- Loss

- Sales

- A business stock turnover time is 9, its average stocks is N60,000. Calculate its cost of goods sold

- N54,000

- N27,000

- N60,000

- N540,000

- The record or book where credit sales could be generated is

- Cash book

- Creditors ledger

- Debtors ledger

- Statement of affairs

Fill in the Blanks

- The number of times a business stock could be replenished is called _______________

- If a business operational margin is 0.2. calculate the mark-up _______________

- The act of recording a business transaction one in the book is called _________________

- The financial summary prepared to ascertain a firm’s opening capital is called ________________

- If a manager is qualified for 7½% commission on profit before the commission is N15,000. Calculate the commission that would accrue to the manager.

Assignment

Essay Type Questions

- The following information was extracted from the book of Olaoni.

N Sales

Opening stock

Closing stock

Expenses

Purchases45,000

20,000

30,000

15,000

25,000You are required to calculate the following:

- Cost of goods sold

- Net profit

- Net profit percentage

- Gross profit percentage

- Stock turnover

- The following is a summary of the bank account of Mary Parker, a retail trader for the year 2008.

| Receipts | N | N |

| Balance b/f Shop takings Payments Creditors Rent and rates drawings | 1,448 34,722 28,364 |

You are given the following additional information:

| 01/01/2008 | 31/12/2008 | |

| N | N | |

| Furniture Stock Debtors Creditors | 1,000 5,260 2,900 3,750 | 1,000 4,380 3,270 3,946 |

During the year, wages amounting to N1,300 and N220 general expenses were paid in cash out of shop takings. All the remaining shop taking were paid into the bank and all other payments were made by cheque.

You are required to prepare:

- Trading, profit and loss account for the year

- A balance sheet as at 31 December, 2008 (SSCE, June 1993).