Share this:

TWO COLUMN CASH BOOK

As the business grow up, the business/firm seems there are necessities of having sometimes to keep their money safe therefore, they usually open the account at bank.

Normally, current account is the kind of account which is preferable by the business owners because;

- It allows to deposit at any time.

- Withdraw even if your account has no enough money/balance (overdraft). You may withdraw more money than what they have.

- Enable to pay his creditors by means of cheque and to collect also from business debtors direct to the bank.

The bank do service by charging the business trader a little cost/fee called bank charges also the issues to the customer bank statement whenever they need or at the end of the month for verifications.

To keep track day to day transactions record business need to bank account whereby two column cash book needed to bank as to maintain two account at once thus cash account and bank account in the same book instead of maintain separate account.

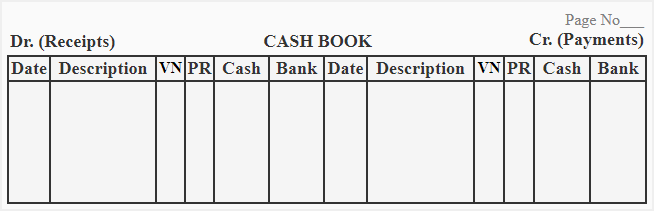

The format of two column cash book

Contra Entries;

Is the French word means opposite/against, means debit and credit done in the same book.

Is where the completion of double entry done in the same book.

Example of the contra entries are:

- If business withdraw cash from bank for office use.

Dr; Cash a/c.

Cr; bank a/c.

- Deposit Cash into bank a/c.

Dr; Bank a/c.

Cr; Cash a/c.

Therefore, to indicate the Contra by use “C” as a symbol in the follow column against the entries as both sides of the cash book.

Example.1

June 1 Balance of Cash in hand 500

Balance at Bank 10,000

2 Received Cash from Mayo 250

3 Paid Chacha by cheque 1,200

4 Received cheque from Minza and banked it 300

6 Received cash from Lily 120

10 Paid rent by cheque 500

15 Paid wages by cash 200

18 Paid cash to bank 100

20 Drew Cash from bank for office use 200

Enter the above transactions in the Cash book and carry down the balance as at 25th June.

Solution

EXERCISE.1

Record the following in the Cash booking of Masai

Feb 1 Opening balance cash Tshs 6,000 Bank Tshs 13,000

4 Paid wages in cash Tshs 1,200

5 Cash sales Tshs 3,000

10 Bought goods by cheque Tshs 1,800

11 paid rent by cheque Tshs 600

19 sent John a cheque for Tshs 600

25 Withdraw Tshs 300 Cash for himself.

Balance off the Cash book and bring down the balance for March.

EXERCISE.2

Record the following in the Cash book of Mwanadada.

April 1 Capital Cash Tshs 4,000 bank 12,000

3 Received Tshs 3,500 cash from Baraza

8 Mwita sent a cheque for Tshs 1,400

13 Paid rent cash Tshs 600

15 Sales by cheque Tshs 11,400

18 Purchases by cash Tshs 1,400

21 Sales by cheque 8,000

26 Purchases by cheque Tshs 10,000

28 Peter paid us Tshs 3,000 cash

29 Paid wages cash Tshs 2,500

30 Paid insurance by cash Tshs 500

Balance off the cash book and bring down the balance for May.