Share this:

POSTING THE SALES JOURNAL TO THE LEDGER

When the sales day book is posted to the ledger each customer is debited with the goods which has been received and the firm whose books are being kept is credited with the sales figure. Every customers has been debited with the good invoiced to him or her, and then,becoming a debtor for that amount.

EXAMPLE.1

Malingumu traders made the following sales during the month of April, record in the sales journal and then post to the ledgers.

1st April sold to Jaluo stores

100 bags of salt @ 5500

50 bags of sugar @ 7,500

10th April sold to Majambozi

15 boxes of cooking fats @ 1700

12 pairs of sandals @ 650

16th April sold to Salome

20 pairs of bed sheet @ 3000

50 T. Shirts @ 3500

20th April sold goods to Kalimanzira worth 36,000 on credit

30th April sold to Baraka

12 bunches of banana @ 2500

10 bags of potatoes @ 6000

Solution1

MALINGUMU TRADER’S

Solution1

MALINGUMU TRADER’S

SALES JOURNAL

DATE | PARTICULARS | F | INVOICE DETAILS | |

1st Apr 10th Apr 16th Apr 20th Apr 30th Apr 30th Apr | JALUO STORES – 100 bags of salt @ 5500 – 50 bags of sugar @ 7,500 MAJAMBOZI – 15 boxes of cooking fats @ 1700 – 12 pairs of sandals @ 650 SALOME – 20 pairs of bed sheet @ 3000 – 50 T. Shirts @ 3500 KALIMANZIRA Goods BARAKA – 12 bunches of banana @ 2500 – 10 bags of potatoes @ 6000 Transferred to Sales A/C Cr. in the general ledger. | 550,000 375,000 25,500 7,800 60,000 175,000 30,000 60,000 | 925,000 33,300 235,000 36,000 90,000 1,319,300 |

DR JALUO TRADERS A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

1st Apr | sales | 92,500 | |||||

DR MAJAMBOZI A/C CR

DATE | DETAILS | F | AMOUNT | DETAILS | F | AMOUNT | |

10thApr | sales | 33,300 | |||||

DR SALOME A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | |

16thApr | sales | 235,000 | |||||

DR KALIMANZIRA A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

20thApr | sales | 36,000 | |||||

DR BARAKA A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

30thApr | sales | 90,000 | |||||

GENERAL LEDGER

DR SALES ACCOUNT CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

30thApr | Balance c/d | 1,319,300 | 30thsept | Sundry debtors | 1,319,300 | ||

1st May | Balance b/d | 1,319,300 |

EXERCISE.1

Enter the following transaction into the sales journal of Mpangala and post to the ledgers.

1st Jan sales to P. Mpali

16 national radio @ 3500

25 record players @ 5200

7th Jan sold some equipment to Uyonga formed associates worth 19650

10th Jan sales to N. Sambamba

60 footballs @ 1760

100 pairs sport shoes @ 6000

90 packets of socks @ 90

15th Jan sold music instruments to Tunsume Ben Band 17,000

19th Jan sold various music instruments to pay Demas month 16,200

25th Jan sold to Madinda Sec School

65 account books @ 500

10 dozen ball paint pencil @ 1200

40 dozen staff ledger @ 80

27th Jan sold forms tools to Hopetended and sons worth 9200

EXERCISE.2

Record the following transaction in the sales day book of Minani and then post to the ledgers .

4th Feb. sales to H. Alindogo

25 boxes of biscuits @ 950

8 cases of beer @ 300

150 bottles of double cola @ 450

9th Feb sold to M. Salub

500kg milk powder worth @ 6

60 cartons soap @ 200

12th Feb sold food worth 1700 to Mr. Chuwa

19th Feb sold goods to:

- Idiasas shs. 7,500

L. Luka shs. 1,200

25th Feb sales to P. Sufiani

5 dozen table knives at T.shs. 8 each knife

200 frying pans set @ T.shs. 70

100 sufuria at @ T.shs 65

27th Feb sold Sandy goods to M. Mchafu ta T.shs. 18,000

28th Feb

sold to K. Kijiko

sold to K. Kijiko

700 bags cement of 50kg at @ T.shs. 85

120 garden Focks @ T.shs. 25

50 shoes valued of T.shs. 30

29th Feb sold summary articles to S. Haruna worth T.shs. 1,660

Solution.QN1

MPANGALA’S

SALES JOURNAL

DATE | PARTICULARS | F | INVOICE DETAILS | INVOICE TOTAL |

1st Jan 7th Apr 10th Jan 15th Jan 19th Jan 25th Jan 27th Jan 31th Jan | P. MPALI – 16 national radio @ 3500 – 25 record players @ 5200 UYONGA – Goods N. SAMBAMBA – 60 footballs @ 1760 – 100 pairs sport shoes @ 6000 – 90 packets of socks @ 90 TUNSUME BEN BAND – Goods VARIOUS MUSIC – Goods MADINDA SEC. SCHOOL – 65 account books @ 500 – 10 dozen ball paint pencil @ 1200 – 40 dozen staff ledger @ 80 HOPITENDED AND SONS – Goods Transferred to sale Cr in the General Ledger. | 56,000 130,000 105,600 600,000 8,100 32,500 12,000 3,200 | 186,000 19,650 714,600 17,000 16,200 47,700 9,200 1,010,350 |

SALES LEDGER

DR P. MPALI A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

1st Jan | sales | 186,000 | |||||

DR UYONGA A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

7th Jan | sales | 19,650 | |||||

DR N. SAMBAMBA A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

10th Jan | sales | 714,000 | |||||

DR VARIOUS MUSIC A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

19th Jan | sales | 16,200 | |||||

DR MADINDA SCHOOL A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

25th Jan | sales | 97,700 | |||||

DR HOPITENDED & SONS A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

27th Jan | sales | 9,200 | |||||

PURCHASES RETURN DAY BOOK OR RETURN OUTWARD JOURNAL

1. What are the reasons which may make you to return goods,

While you had purchased from supplies?

(i) Damaged of goods in transits

(ii) Expired of goods

(iii) Over supplies.

(iv) Low quality.

(v) Not of the sample ordered.

(vi) Not of the color ordered.

2. Goods sold and bought on credit may be return due to the following reasons.

(i) Wrong types

(ii) Wrong color

(iii) Not the sample ordered

(iv) Incomplete of goods

(v) Damaged in transit

(vi) Expired of goods

When goods are returned to the supplies prepared a document called CREDIT NOTE to inform the buyer that the half credit his account.

It is a reduction of the debit (claim) or it rectifies/ adjusts on over changed amount.

It is a reduction of the debit (claim) or it rectifies/ adjusts on over changed amount.

A record of the return of goods / purchases on credit is kept in a returns outwards journal (or purchased returns journal).

EXAMPLE.1

Enter the following items in Manjani’s purchases returns day book and post to the ledger.

7th Jan return one bag of rice of R.T.C

Kilimanjaro Tshs. 500 not suitable for consumption.

10th Jan returns two boxes cooking fat @ Tshs 320 to Manji Xsons

& Lxd, not of the type ordered.

2 bags of beans at Tshs. 1000 was out of use

11th Jan returns one pair bed sheets Tshs. 170 and two shift @ Tshs. 350 to Moshi Traders poor qualities

MANJANI’S

PURCHASES RETURNS DAY BOOK

DATE | PARTICULARS | F | INVOICE DETAILS | INVOICE TOTAL |

7th Jan 10th Jan 11th Jan 31st Jan | R.T.C KILIMANJARO SHOP 1 bag of rice T.shs 500 MANJI AND SONS LTD 2 boxes of cooking fat @ T.shs. 320. 2 bag of beans @ T.shs. 1,000 MOSHI TRADERS 1 pair bed sheet of @ 170 2 shift @ 350 Transferred to the Return outward A/C Cr. In the general ledger. | P.R.1 P.R.2 P.R.3 | 640 2,000 170 700 | 500 2,640 870 4,010 |

PURCHASES RETURN LEDGERS.

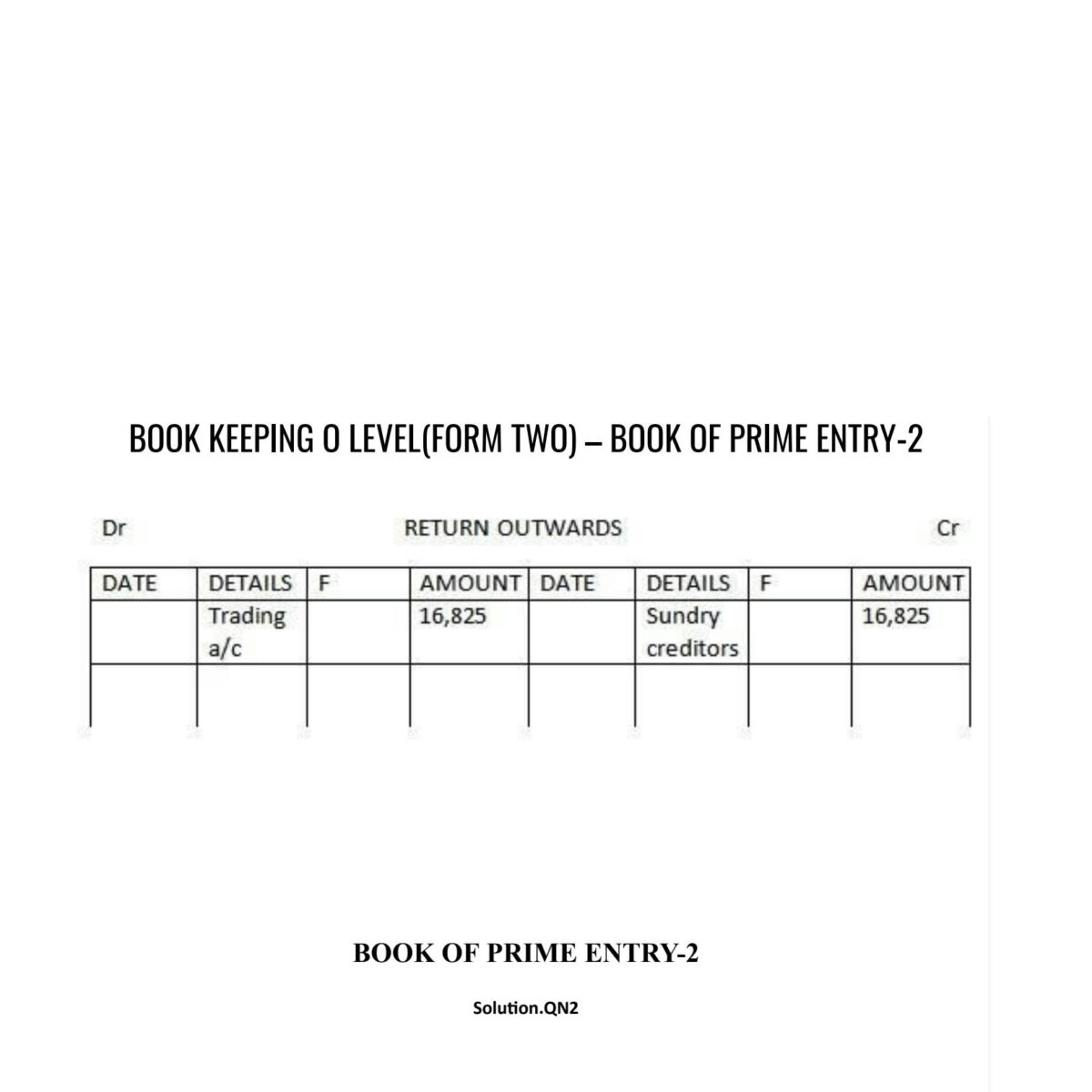

DR R. T. C. KILIMANJARO SHOP A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

7th Jan | Purchases return | 500 | |||||

DR MANJI AND SONS LTD A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

10th Jan | Purchases return | 2,640 | |||||

DR MOSHI TRADERS A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

15th Jan | Purchases return | 870 | |||||

EXERCISE.1

Enter the following transaction in the purchases returns day book and post to the ledgers.

3rd Mach returns to Wale wetu

5 pairs of boots of @ T.shs. 200 not of the type orderd

10 pair of sandals of @ T.shs 35 wrong size

5th March Return to Mkwanda

12 sponje mattress @ Tshs. 600, poor quality

2 safari beds @ Tshs. 800, damaged in transit

12th March return to Sangura

250 metres vitenge material @ T.shs 35, not up to started ordered

22nd March Return to Morogoro Shops Company

300 pair of shoes @ T.shs 450, not of the size ordered

150 pairs children shoes @ T.shs. 250, a pair not of type ordered

200 dozen baby nephis at @ T.shs. 200, not of the colour order.

Solution

PURCHASES RETURNS DAY BOOK

DATE | PARTICULARS | F | INVOICE DETAILS | INVOICE TOTAL |

3rd Mar 5th Mar 12th Mar 22ndMar 31stMar | WALE WETU – 5 pairs of boots of @ T.shs. 200 – 10 pair of sandals of @ T.shs 35 MKWANDA – 12 sponje mattress @ Tshs. 600 – 2 safari beds @ Tshs. 800 SANGURA – MOROGORO SHOP COMPANY – 300 pair of shoes @ T.shs 450 – 150 pairs children shoes @ T.shs. 250 – 200 dozen baby nephis at @ T.shs. 200 Transfer purchases returns A/C by Cr the general ledger . | 1,000 350 7,200 1,600 8,750 135,000 37,500 40,000 | 1,350 8,800 8,750 91,000 109,900 |

POSTING TO THE LEDGERS.

DR WALE WETU A/C CR

DATE | F | AMOUNT | DATE | DETAILS | F | AMOUNT | |

3rd Mar | Purchases return | 1,350 | |||||

DR MKWANDA A/C CR

DATE | DETAILS | F | AMOUNT | DETAILS | F | AMOUNT | |

5th Mar | Purchases return | 8,800 | |||||

DR SUNGURA A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

12th Mar | Purchases return | 8,750 | |||||

DR MOROGORO SHOP COMPANY A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

22th Mar | Purchases return | 91,000 | |||||

GENERAL LEDGER

DR PURCHASES RETURNS A/C CR

DATE | DETAILS | F | AMOUNT | DATE | DETAILS | F | AMOUNT |

31th Mar | Balance c/d | 31st Mar | Sundry creditors | 109,900 | |||

1stApr | Balance b/d | 109,900 |

EXERCISE.2

Enter the following transaction in NAMSHITUS purchases day book, purchases returns day book and post to the ledgers.

1st May Bought 10 bags of beans @ T.shs. 600 from National Distributors Ltd.

4th May purchase 2 dozen of cooking oil of @ T.shs. 50 from GEFCO

5th May return one bag of beans to National Distributors Ltd

8th May Bought 10 dozen of bed sheet from Kilimanjaro Text Tile @ T.shs. 2,2

00

00

10th May Returned to GEFCO half a dozen cooking oil as they were not the quality ordered

15th May purchased from GEFCO 100 dozen of baby milk @ T.shs 600

20th May returned one dozen bed sheet to Kilimanjaro Text tiles as they were poor quality

25th May returned 5 dozen of baby milk to GEFCO spoilt in transit

26th May Purchased 20 dozen bed sheet from Kilimanjaro Text Tiles @ T.shs. 2,200

28th May reformed 5 dozen bed sheets as they were not of the size ordered from Kilimanjaro Textiles